Not withdrawing your RMD can incur a penalty of up to 50% of the undistributed amount. Did you know that? This is why it is crucial to understand the rues for Required Minimum Distributions (RMD) at your applicable age. Check through the following paragraphs to make sure you can get the most from your Gold IRA without being penalised.

Key Takeaways

- Gold IRAs require you to start taking Required Minimum Distributions (RMDs) at age 73, not 72, due to recent legislative changes.

- Failing to withdraw the required RMD can lead to a hefty penalty of up to 50% of the undistributed amount.

- RMDs can be taken in cash or as physical gold, but it’s crucial to understand the tax implications of each choice.

- Inherited Gold IRAs have different rules, including a 10-year withdrawal requirement for non-spouse beneficiaries.

- Calculating your RMD accurately involves using IRS life expectancy tables, which can be done using online tools for ease.

Why Age 73 Is Crucial for Gold IRA RMDs

When it comes to securing financial freedom during retirement, understanding the rules around Required Minimum Distributions (RMDs) for Gold IRAs is essential. These distributions are not just arbitrary; they’re a mandate by the IRS to ensure taxes on your retirement savings are eventually paid. So, why is age 73 so crucial? Because that’s when the IRS expects you to start withdrawing from your Gold IRA. This change from the previously known age of 72 is due to recent legislation that aims to extend the time for tax-deferred growth.

Reaching the age of 73 is a milestone for Gold IRA holders. It marks the point at which you must begin taking RMDs, regardless of whether you need the money or not. This requirement ensures that you eventually pay taxes on your tax-deferred retirement savings. Failing to take your RMD can lead to severe penalties, making it crucial to understand and comply with these rules.

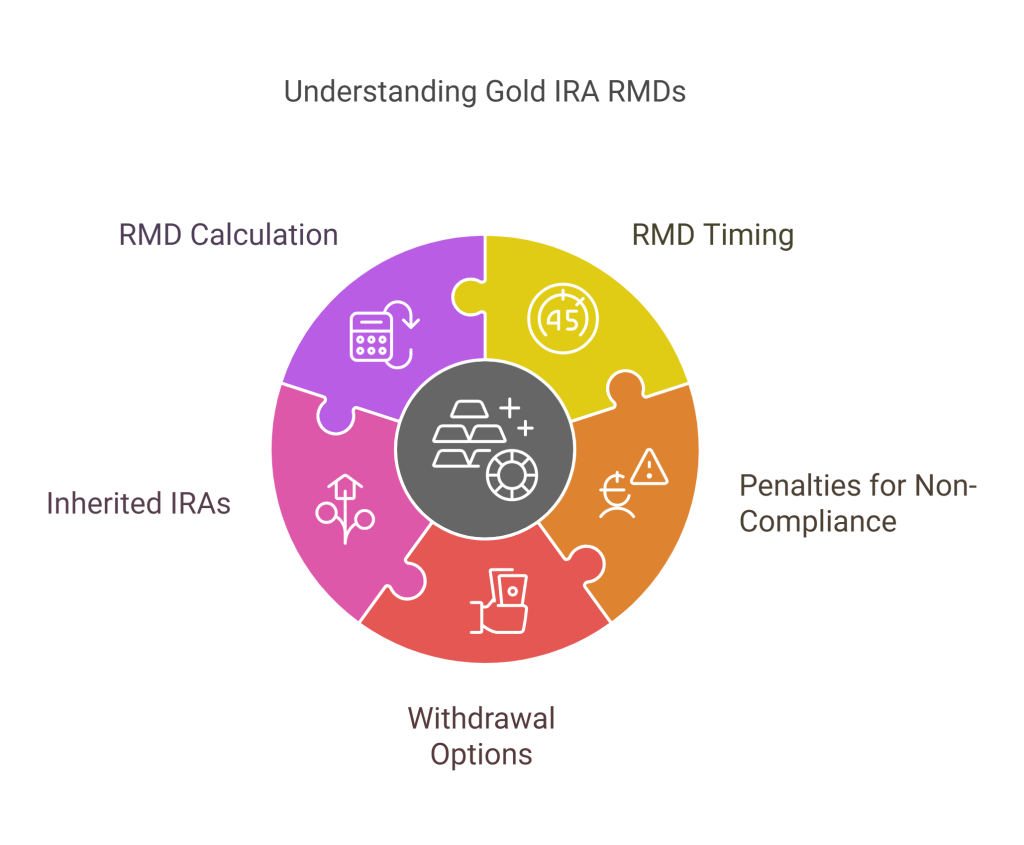

Understanding Required Minimum Distributions for Gold IRAs

RMDs are a way for the IRS to ensure that people pay taxes on their retirement savings. These distributions are the minimum amount you must withdraw from your retirement account each year, starting at age 73. For Gold IRAs, this means you need to start planning how you’ll take these distributions—whether in cash or in physical gold. Both options have their own tax implications and logistical considerations.

It’s important to note that RMDs are calculated based on your account balance at the end of the previous year and your life expectancy. The IRS provides tables to help with these calculations, making it easier for you to determine the amount you need to withdraw. However, it’s always wise to consult with a financial advisor to ensure you’re meeting your obligations and optimizing your financial strategy.

Changes in Legislation Impacting RMD Age

Recent legislative changes have shifted the RMD age from 72 to 73, allowing for an extra year of tax-deferred growth. This change is part of a broader effort to modernize retirement laws and provide more flexibility to retirees. Understanding these changes is vital, as they directly impact your retirement planning strategy.

Besides that, these changes mean that retirees have more time to let their investments grow before being required to withdraw. This can be particularly beneficial for those who do not immediately need the funds and wish to maximize their retirement savings. However, it also requires a recalibration of withdrawal strategies to align with the new rules.

Core Benefits of Investing in a Gold IRA

Investing in a Gold IRA offers several benefits, particularly in terms of diversification and protection against inflation. Gold has historically been a stable store of value, providing a hedge against economic downturns and currency devaluation. This makes it an attractive option for those looking to preserve wealth over the long term.

Moreover, Gold IRAs offer tax advantages similar to other retirement accounts. Contributions may be tax-deductible, and the growth of your investment is tax-deferred until you start taking distributions. These benefits, combined with the security of owning physical gold, make Gold IRAs a compelling choice for many retirees.

Life Expectancy Factors and IRS Tables

When calculating your Required Minimum Distribution (RMD) for a Gold IRA, life expectancy factors play a crucial role. The IRS provides tables that list life expectancy figures based on your age. These tables help determine the amount you need to withdraw annually. The idea is to spread your withdrawals over your expected lifetime, ensuring that you don’t outlive your savings.

To use these tables, you’ll need to know your account balance as of December 31 of the previous year. Divide this balance by the life expectancy factor from the IRS table that corresponds to your age. This calculation gives you the minimum amount you must withdraw for the year. Remember, it’s always wise to double-check your calculations or consult a financial advisor to ensure accuracy.

Example Calculation for Gold IRAs

Let’s walk through a simple example to illustrate how RMDs are calculated for a Gold IRA. Suppose you are 73 years old and have a Gold IRA balance of $200,000 as of December 31 of last year. According to the IRS Uniform Lifetime Table, your life expectancy factor is 24.7. To calculate your RMD, divide $200,000 by 24.7, which equals approximately $8,097.16. This is the minimum amount you must withdraw for the year.

This example highlights the importance of understanding how RMD calculations work. It’s not just about compliance with IRS rules; it’s also about effective financial planning to ensure your retirement savings last as long as you need them.

Tools and Resources for Accurate Calculations

Fortunately, you don’t have to calculate RMDs manually. Several online tools and calculators can simplify this process. These tools allow you to input your account balance and age, then automatically calculate your RMD based on the latest IRS tables. This can save you time and reduce the risk of errors.

Besides online calculators, consulting with a financial advisor is a smart move. Advisors can provide personalized guidance, taking into account your overall financial situation and goals. They can also help you navigate any changes in tax laws or IRS rules that might affect your RMD calculations.

Options and Strategies for Taking RMDs from a Gold IRA

When it comes to taking RMDs from a Gold IRA, you have options. You can choose to take distributions in cash or in-kind, meaning you can withdraw physical gold. Each option has its own implications, so it’s essential to understand them fully before making a decision. For more insights, consider reading about diversifying with a Gold IRA.

Taking RMDs in Cash vs. Physical Gold

Taking RMDs in cash is straightforward. You sell enough gold to meet the RMD amount and take the proceeds as a distribution. This option is convenient but may involve selling gold at a less-than-ideal time, depending on market conditions.

Alternatively, you can take your RMD in-kind by withdrawing physical gold. This option allows you to keep your gold holdings intact, but you’ll need to manage the logistics of storing and insuring the physical gold. Additionally, the fair market value of the gold at the time of withdrawal counts towards your RMD, so it’s crucial to keep accurate records. For more details, you can explore the best way to buy physical gold for your IRA.

Balancing Your Portfolio While Meeting RMD Requirements

Meeting RMD requirements doesn’t mean you have to disrupt your entire investment strategy. By planning carefully, you can balance your portfolio while still complying with IRS rules. Consider your overall asset allocation and how your RMDs fit into your long-term financial goals.

For example, you might choose to take RMDs from underperforming assets or those that have appreciated significantly. This approach allows you to maintain a balanced portfolio while fulfilling your RMD obligations. Remember, the goal is to ensure your retirement savings continue to support your lifestyle for years to come.

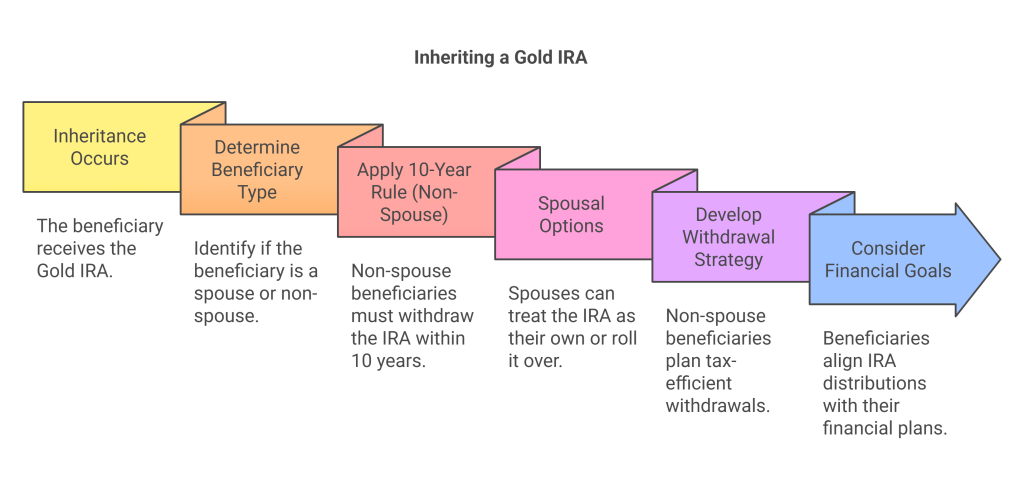

Impacts of Inheriting a Gold IRA

Inheriting a Gold IRA comes with its own set of rules and considerations. Whether you’re a spouse or a non-spouse beneficiary, understanding these rules is crucial for effective estate planning and financial management.

Understanding the 10-Year Withdrawal Rule

For non-spouse beneficiaries, the IRS requires that the entire balance of an inherited Gold IRA be withdrawn within 10 years of the original owner’s death. This rule applies regardless of the beneficiary’s age, meaning you need to plan how you’ll take these distributions over the decade.

One strategy is to spread withdrawals evenly over the 10-year period to minimize the tax impact. Alternatively, you might choose to take larger distributions in years when your income is lower, thereby reducing your overall tax liability. For more information on handling these distributions, visit Noble Gold.

Special Considerations for Spousal Beneficiaries

Spousal beneficiaries have more flexibility when inheriting a Gold IRA. They can choose to treat the IRA as their own, delaying RMDs until they reach age 73. This option allows for continued tax-deferred growth, which can be advantageous if the spouse doesn’t need the funds immediately.

Alternatively, a spouse can roll the inherited IRA into their own IRA, thereby consolidating accounts and simplifying management. This decision should be based on the couple’s overall financial strategy and long-term goals.

Strategies for Non-Spouse Heirs

Non-spouse heirs face different challenges when inheriting a Gold IRA. The 10-year withdrawal rule means they need to plan carefully to manage the tax implications of these distributions. One approach is to work with a financial advisor to develop a strategy that minimizes taxes while meeting financial goals.

Additionally, non-spouse heirs should consider how these distributions fit into their broader financial picture. For example, they might use the funds to pay down debt, invest in other opportunities, or fund major life events like education or a home purchase. The key is to make informed decisions that align with long-term financial well-being.

Final Thoughts on Gold IRA RMDs

Understanding the rules and requirements for Required Minimum Distributions (RMDs) is crucial for anyone with a Gold IRA. These distributions are not just a legal obligation; they are a key part of your retirement planning strategy. By starting at the right age, calculating accurately, and choosing the best method for taking your RMDs, you can ensure that you maximize the benefits of your Gold IRA while minimizing any potential risks.

Maximizing Benefits and Avoiding Risks

- Start planning for RMDs well before reaching age 73 to avoid last-minute decisions.

- Consider both cash and in-kind distributions to see which aligns best with your financial goals.

- Consult with a financial advisor to ensure your RMD strategy fits your overall retirement plan.

- Stay informed about any changes in legislation that could affect your RMDs.

- Keep accurate records of your distributions to simplify tax reporting and compliance.

Remember, the goal is not just to comply with IRS rules but to make strategic decisions that enhance your financial security in retirement. Taking the time to understand your options and plan accordingly can make a significant difference in your financial well-being.

Besides that, it’s essential to stay flexible. As life circumstances change, so might your RMD strategy. Being adaptable ensures that your financial plan remains robust and responsive to new challenges and opportunities.

Finally, don’t underestimate the value of professional advice. Financial advisors can provide insights and recommendations tailored to your specific situation, helping you navigate complex rules and make informed decisions.

Staying Informed on Changes to Legislation

The world of retirement planning is ever-evolving, with new laws and regulations emerging regularly. Staying informed about these changes is crucial to ensuring your retirement strategy remains effective and compliant. This is particularly true for Gold IRAs, where legislative shifts can directly impact your RMDs and overall financial planning.

One way to stay informed is by subscribing to financial news sources and updates from trusted financial institutions. These resources can provide timely information on any changes that might affect your retirement accounts.

Additionally, consider joining retirement planning forums or groups. These communities can offer valuable insights and support, allowing you to learn from others’ experiences and share your own. Engaging with like-minded individuals can provide a broader perspective on retirement planning and keep you up-to-date with the latest trends and strategies.

Gold IRA Required Minimum Distribution FAQs

Many people have questions about Gold IRA RMDs, and it’s essential to address these to ensure clarity and confidence in your retirement planning.

One common question is about the penalties for missing an RMD deadline. The IRS imposes a hefty penalty of up to 50% of the amount not withdrawn, so it’s crucial to adhere to the rules and take your RMDs on time.

“Failing to take your RMD can result in a penalty of up to 50% of the undistributed amount.”

Another question is whether RMDs can be taken in the form of physical gold. Yes, they can, but it’s essential to understand the implications, such as the need for proper storage and the potential impact on your portfolio balance.

What happens if I don’t take my RMD on time?

If you fail to take your RMD by the deadline, the IRS can impose a penalty of up to 50% of the amount not withdrawn. This penalty underscores the importance of adhering to RMD rules and planning your distributions carefully.

Can RMDs be taken in the form of physical gold?

Yes, you can take RMDs in the form of physical gold. However, you must ensure the fair market value of the gold at the time of withdrawal meets the RMD requirement. Additionally, consider the logistics of storing and insuring the physical gold.

How does inheriting a Gold IRA affect my taxes?

Inheriting a Gold IRA can have significant tax implications. Non-spouse beneficiaries must withdraw the entire account balance within 10 years, potentially leading to a higher tax burden. It’s essential to plan these withdrawals strategically to minimize tax impact. For more information on managing your inherited IRA, consider reviewing a trustworthy IRA custodian choice guide.

What are the penalties for missing an RMD deadline?

The penalty for missing an RMD deadline is severe. The IRS can charge up to 50% of the amount not withdrawn. This penalty highlights the importance of understanding and complying with RMD rules to avoid unnecessary financial setbacks.

Do Roth Gold IRAs have the same RMD requirements?

No, Roth Gold IRAs do not have the same RMD requirements. During the account holder’s lifetime, Roth IRAs are not subject to RMDs, allowing the funds to grow tax-free without mandatory withdrawals. This can be a significant advantage for those looking to maximize their retirement savings.

“Roth Gold IRAs do not require RMDs during the account holder’s lifetime, offering tax-free growth potential.”

Understanding these nuances can help you make informed decisions about your Gold IRA and ensure your retirement strategy is as effective as possible.

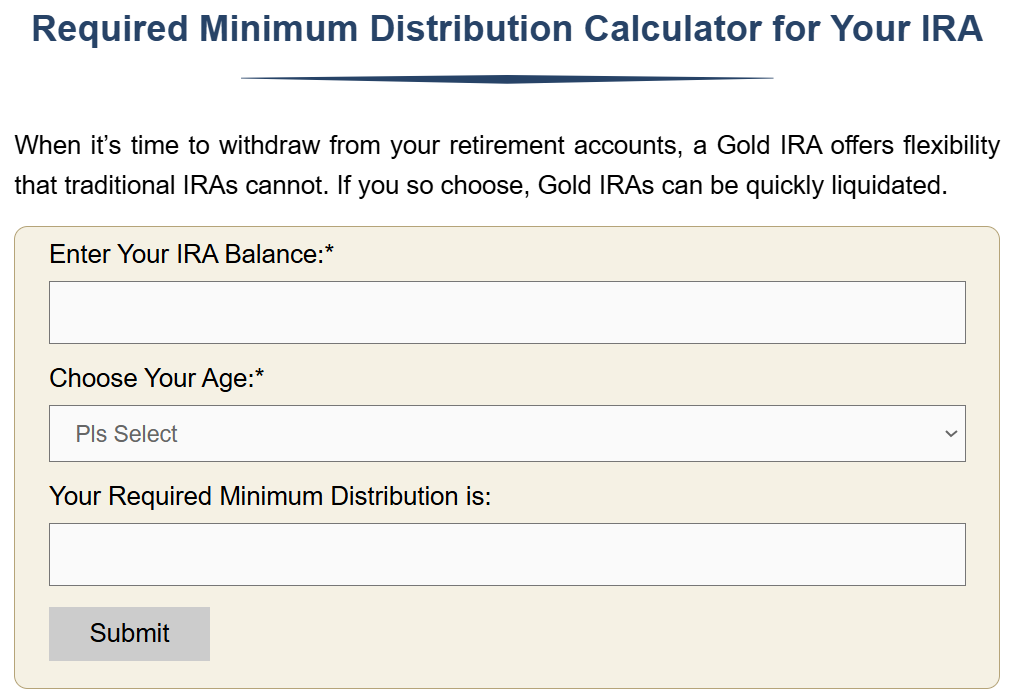

Want to find out your Required Minimum Distributions estimate?